Not long at all. During the last freight cycle, there was a 56-day period when truckload spot rates increased by 25.6% and a 59-day period when rates fell by 15.1%.

Right now, transportation rates are unseasonably low and capacity is plentiful across most modes of traffic, from North America truckload to trans-Pacific ocean container shipping.

But shippers shouldn’t become complacent in the trough of the cycle: Historically, the market has flipped faster than shippers can adjust, to the detriment of their supply chains, transportation budgets and customer relationships. Instead, the trough is the time to work through software procurement processes that will put you ahead of the next cyclical inflection.

After spot rates have spiked by 25% and your contracted carriers aren’t accepting many of your least desirable shipments, it’s too late to start looking for pricing solutions, freight data and automation layers to figure out what’s going wrong. Enterprise software procurement cycles are lengthy and complex, implementation can take time, and even the smoothest integrations benefit from some change management and training.

Even if they respond quickly, by the time enterprises like food and beverage brands, retailers, paper and packaging companies, and industrial manufacturers can leverage a new digital supply chain tool across their organization, the damage has been done.

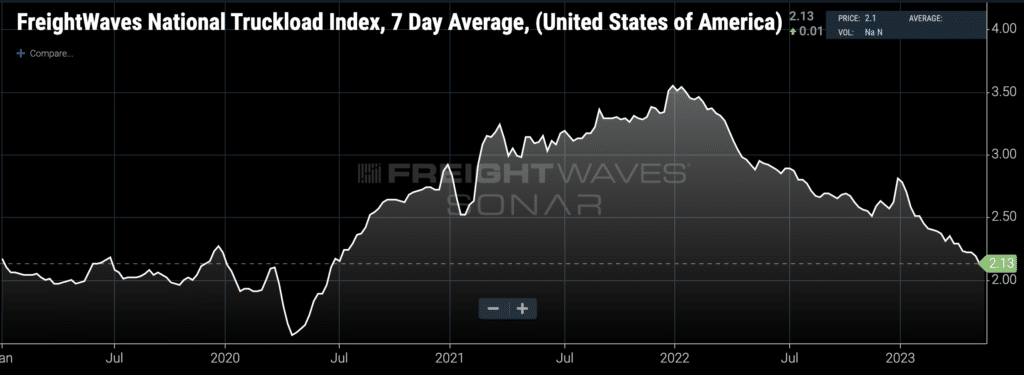

To illustrate just how quickly the freight market can turn, let’s review a little history: the middle of 2020. Lockdowns had put a chill on business and consumer activity across the country, and it was unclear how the U.S. consumer would react to an unprecedented level of uncertainty and risk. On April 19 of that year, FreightWaves’ National Truckload Index, a fuel-inclusive national average truckload spot rate, bottomed at $1.56 per mile, a rock-bottom rate well below most carriers’ operating costs.

But then consumers started to buy, stock-outs broke out in retail locations across the country, and distribution centers rushed to fulfill demand. The NTI climbed to $1.72 per mile by May 17, a 10.2% increase in less than a month.

By June 14, the NTI had jumped to $1.96 per mile, a 25.6% jump in just 56 days since the market bottom. By that time, a large shipper analyzing its own paid rates would have just seen the market bottom and would still have no idea what was about to happen. The trucking market kept ripping higher all summer: By July 19, the NTI was at $2.24, by Aug. 16 it had climbed to $2.42, and by Sept. 30, near the lead-up to peak season, spot rates were already at $2.64 per mile, a 69.2% jump from the market bottom in April.

(The National Truckload Index is FreightWaves’ truckload spot rate index, published daily from billions of dollars of transactions. To learn more about FreightWaves SONAR, click here.)

Why does the market change so quickly? The balance of supply and demand, or transportation capacity and freight volumes, ebbs and flows slowly but is almost never static. When supply and demand are in balance, the market is like a roller coaster car at the top of a hill, waiting for a push to determine which direction it will roll down. Often external catalysts like natural disasters, trade agreements, regulations and government spending can accelerate upcycles.

But shippers, brokers and carriers can experience the same high rates of change and volatility in the market during downturns, too — not just the unprecedented volatility of the early pandemic. The National Truckload Index had a recent peak at $2.83 per mile on Jan. 3 but started falling fast. A month later, the national average spot rate had dropped to $2.51, and by March 3, the rate had slid further to $2.40 per mile. In 59 days, then, the national average rate fell 15.1%. Individual lanes were even more volatile.

Financial analysts and industry observers have commented that today’s truckload spot rates — the NTI is at a very low $2.13 per mile — are unsustainable given inflation in carriers’ operating costs and deteriorating asset utilization. While some shippers are breathing a sigh of relief, transportation markets are potentially being set up for a long, deep trough, one that bleeds too much capacity out of the market. When the market turns again, the melt-up will be sudden.

Supply chain leaders are using the quiet market to make strategic investments and improve the responsiveness and resilience of their operations. An obvious place to go is market intelligence and data analytics platforms like FreightWaves SONAR that can accelerate the propagation of data through enterprise shipper organizations, enabling them to react to supply chain volatility in real time.

To learn more about FreightWaves SONAR, click here.