The pandemic has sent the retail industry on a K-shaped trajectory — the final straw that has sent many retail chains into bankruptcy while also contributing to a surge in sales for many of the leading chains. The difference has been not only offering products that customers are seeking, but also the impact of scale and supply chain sophistication that many smaller chains could not match.

Supply chain sophistication promises to become even more important going forward as Amazon has raised consumers’ expectations for service that should be both immediate and free at the same time. Meanwhile, national-branded consumer goods companies gained share from private labels during the pandemic and many are launching direct-to-consumer and subscription services looking to reduce their reliance on retail and reach their most loyal customers.

Those challenges and others have put pressure on retailers to build omnichannel offerings that “meet customers where they are.” That has also increased the pressure on retailers to keep other freight and logistics costs low with more capital and expense being dedicated to the development of new omnichannel strategies.

In this report, we discuss several use cases for retailers to utilize the FreightWaves SONAR platform to increase efficiency throughout their supply chains.

Those use cases include:

In addition, we discuss what the financial impact can be on a large retailer that is able to reduce freight spend. We estimate that retailers with average margins and an average relative freight spend could save $225 for every $1 million in retail revenue by improving freight efficiencies by 1%. That scales nicely when put in the context of multibillion dollar retail chains as we illustrate in this report.

As disorienting as the past year and a half have been for everyone, few industries have experienced as much upheaval as retail.

The recent economic recovery has often been described as “K-shaped,” or a bifurcated recovery by segment. That description is particularly apt to describe the retail industry. Numerous retailers were forced into bankruptcy protection in the last year and a half and/or closed stores for good. Of course, during that same period, many retailers performed extremely well. The retailers that performed the best over the past year were generally the ones that sold essential goods, such as food, or benefited from the trends of the hour, such as home repair. In addition, the best-performing retailers leveraged their scale, their technological capabilities and the cost-mitigation measures they already had in place. They were also the most flexible in adapting to the fast changes that took place. In short, the retail shakeout left the industry with a smaller number of sophisticated players.

The “better” retailers survived the pandemic, but challenges abound. Here is a small sample of the issues that retailers are contending with:

Those issues are likely to give rise to permanent changes in retailers’ supply chain:

What those changes to the retail industry all have in common is that they are in response to higher expectations for customer service.

Amazon ushered in a new era in which service, rather than price, was the biggest determinant of retail logistics strategy. Amazon’s logistics practices were never “low-cost,” but instead increased consumers’ expectations for service levels and forced other retailers to up their level of service. Put differently, Amazon’s logistics strategy has been a high-cost/high-service strategy, but delivered at a lower cost (for that high level of service) than was possible by its less nimble competitors.

As a result, pressure has been applied on the broad retail industry to improve its customer service to levels where the gap with Amazon is, if not at parity, at least less noticeable. Other retailers may not be able to provide the extension-of-your-thoughts delivery in one hour that Amazon can, but with sufficient investment they can likely provide delivery or store pickup on specialized goods in a way that is more convenient than what was available before.

E-commerce had been growing ~9% per year before the pandemic and experienced an acceleration that arguably brought forward e-commerce growth that might have otherwise taken another four to six years to achieve. The expectation that consumers’ e-commerce habits will “stick” post-COVID is about the least controversial opinion that one can express on the pandemic.

Where does this mean for retailers’ use of SONAR?

On page 2, we brainstormed 10 challenges that retailers are more heavily facing now and eight ways in which we believe the retail industry and retailers’ logistics are changing. From those lists, it’s clear that we don’t have all the answers. But putting ourselves in the perspective of a retailer, we recommend utilizing SONAR in the following ways to improve supply chain efficiency.

Those use cases can be categorized as supporting day-to-day operations to minimize freight costs and those use cases are our focus in the coming pages. In addition, SONAR data could be used by retailers for strategic and longer-term decision-making, such as deciding where to locate warehouses and fulfillment centers.

Retail use case No. 1: Monitoring import volume, global trade and port activity for evidence of supply chain disruption.

See the tsunami of volumes before and after they arrive into the U.S.

View ocean volumes before and after they arrive at a country-to-country level, port level or on a lane level to visualize ocean container demand at the most granular level. You may hear “from sources overseas” that volumes have reached an all-time high, but having an objective third-party source that can confirm what you may suspect as “hearsay” provides you with the additional, actionable insight and confidence you need to drive key decisions for your supply chain. Then, as the volumes arrive into the U.S., have the confidence of knowing the exact volumes that each port handled to identify key market-share trends across U.S. ports.

Monitor container volumes at origin into the future to gain insight into demand-driven pressures on capacity (and rates).

With SONAR, users have the ability to monitor containerized ocean freight volumes at origin to better understand how demand is affecting pressures on capacity and rates. With more than two years of history, and a seven-day leading projection of container volumes expected to leave a specific origin port, you have the ability to monitor and understand whether demand is putting pressure on capacity and rates.

Identify surface transportation trends being driven by U.S. containerized imports.

How is the rest of the market responding to the challenges being brought forth from an overwhelming surge of containerized imports flooding U.S. ports? Are containers being transloaded into 53-foot dry vans and trucked from portside markets, or are the rails capturing more market share of outbound surface shipments to the inland markets around the U.S.? SONAR data can identify tight relationships such as U.S.-bound containerized imports from China driving 53-foot dry van volumes across the U.S.

Visualize critical imbalances in capacity in real time.

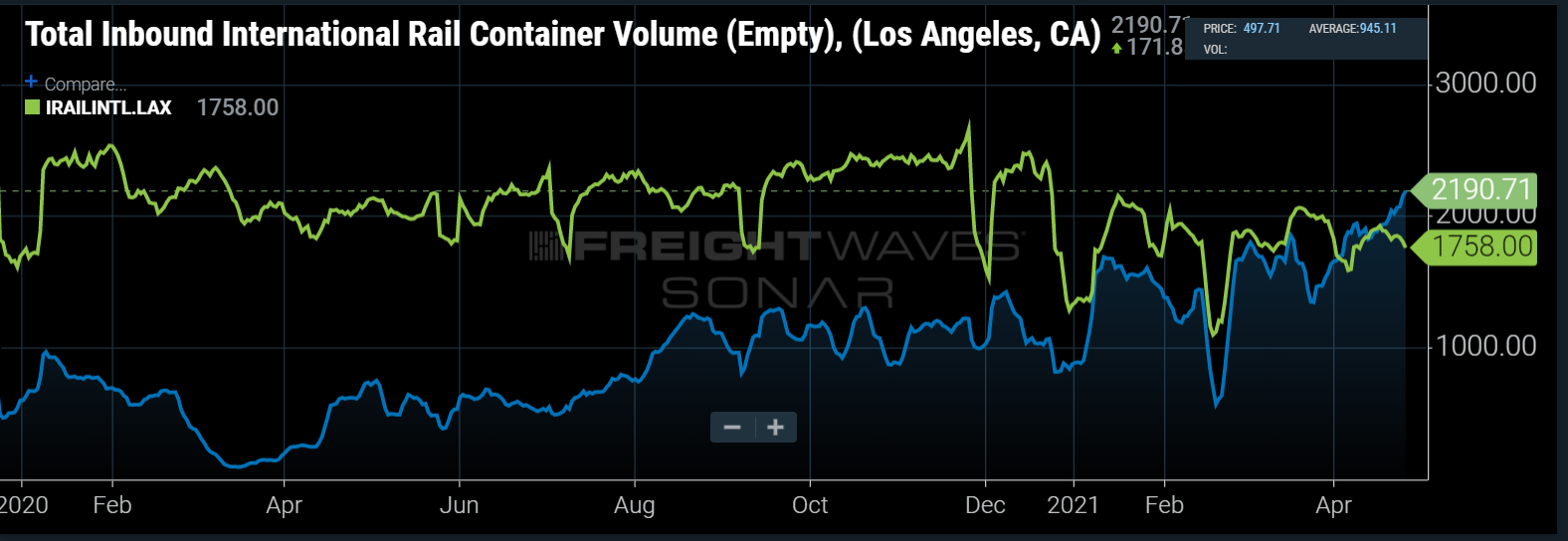

With SONAR, you have the ability to monitor international container volumes (and whether they are loaded or empty) on the rail to identify important trends in demand and capacity within the key inland container markets throughout the entire U.S. When more empty international containers are moving into the Los Angeles market than loaded containers, you will know that the repositioning of containers by ocean carriers has reached a critical level. Not only does this enable you to prepare for the storm ahead, but it also enables you to provide key insights to the rest of the team to better explain the seriousness behind specific issues and “warning signs” within the market.

Retail use case No. 2: Evaluating freight flows for conversion from for-hire to private fleets or conversion from one-way truckload to dedicated.

The conversion from the for-hire market to a private fleet or one-way truckload moves to dedicated lanes removes the volatility that the transportation industry typically faces. The removal of the volatility allows consistent expectations in freight spend as well as service levels that private and dedicated fleets offer shippers compared to that of the for-hire truckload market, especially in one-way, or spot, moves.

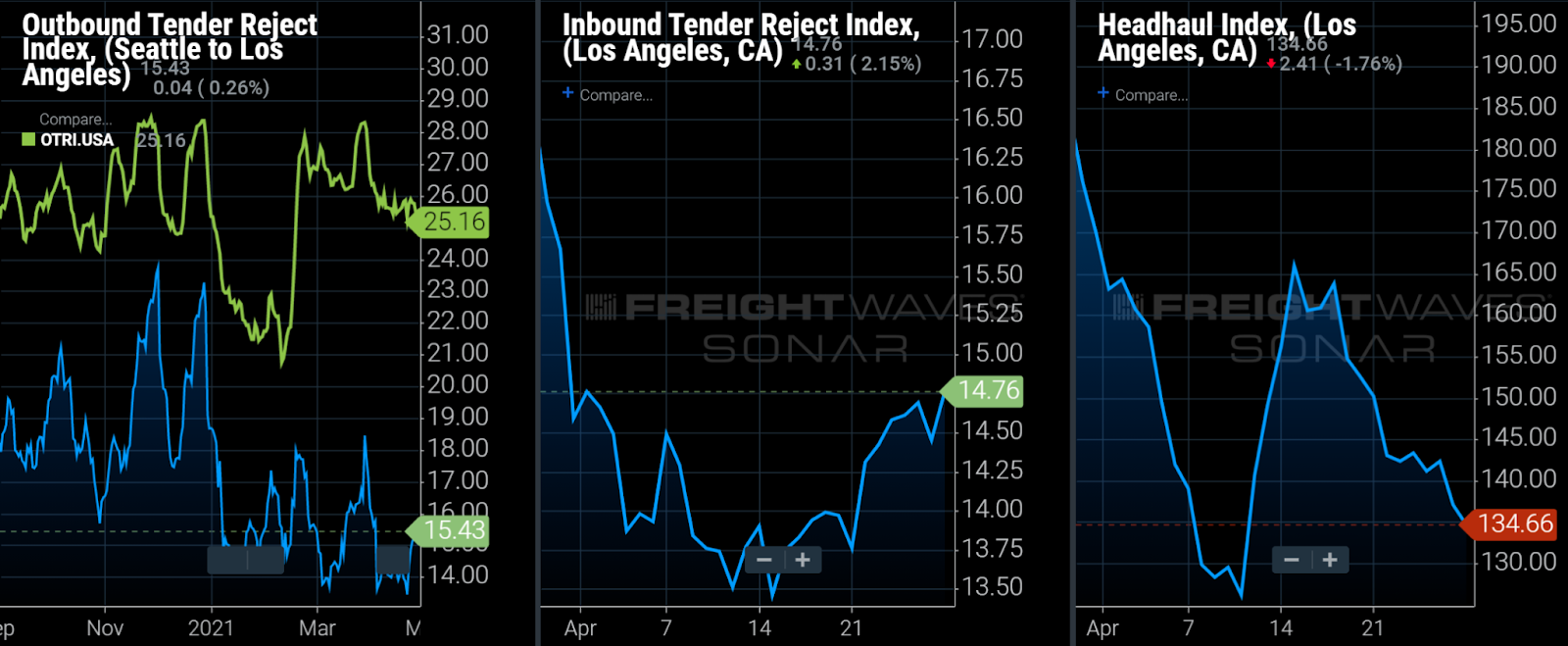

The COVID-19 pandemic brought upon unprecedented volatility in the freight industry, with volume levels, as measured by the Outbound Tender Volume Index (OTVI), reaching the lowest seasonal levels in April 2020 since the inception of the data set before surging throughout the rest of the year, leading to numerous record highs, peaking on Black Friday. The capacity side of the equation is much more opaque, however the Outbound Tender Reject Index (OTRI) measures relative capacity within the markets.

The most volatile markets in the country are made up of some of the smallest freight markets in the country, making them less than ideal for conversion to a private fleet. The largest 15 freight markets in the country make up 36.034% of total tender volumes and the top 25 markets make up more than 50% of total freight volume in the country.

When putting an example shipper network into FreightWaves’ Supply Chain Intelligence (SCI) platform, the platform benchmarks rates against the overall market rate as well as the peer group, in this case retail. The platform displays how the current benchmark rate matches up against both the market rate and peer group comparison along a given lane while also giving a score on the lane between zero and 100, with the higher the number being the more difficult to cover over time.

In the example below, there are a few lanes that would be beneficial to convert to a private fleet or dedicated service given the low SONAR score, meaning that the lanes are quite difficult to cover over time, while other lanes listed below don’t receive the same benefit for conversion.

Low Lane Score = difficult lane for shippers to manage

(Source: FreightWaves SCI)

Lane 1: Springfield, Illinois (Taylorville market) to Harrisburg, Pennsylvania

The lane overall is difficult to cover due to the volatility of load acceptance in Springfield as the benchmark rate is significantly below the overall market and peer group rate along the lane. The overall score currently sits at 6, though the destination market, Harrisburg, is one of the largest freight markets in the country, accounting for more than 3% of overall tenders in the country.

The use of a private or dedicated fleet will allow for a shipper to offset the volatility in the Taylorville market, a really small market compared to nearby markets like St. Louis, Indianapolis and Chicago.

Lane 2: Reading, Pennsylvania to Washington, D.C.

The Reading-to-Washington lane is difficult to cover given the short distance, ~150 miles, and the lack of carriers willing to enter the D.C. market, which has very limited outbound freight. Additionally, the benchmark rate is more than 50% below what the peer group is paying, making it difficult to secure the capacity needed to service the lane.

The use of a private fleet or dedicated service as opposed to moving loads into the spot market along this lane will keep costs low when freight volumes out of Reading turn up instead of fight carriers to leave the larger surrounding areas like Harrisburg and Allentown, Pennsylvania.

High Lane Score = relatively easy lane for shippers to manage

(Source: FreightWaves SCI)

Two lanes where the conversion to a private fleet doesn’t seem as useful is from Phoenix to Santa Ana, California, and Stockton, California, to Chicago. The lanes have volume density as well as the destination market being a major freight hub. The result is really high SONAR scores, 75 and 71, signifying the relative ease to cover the loads along the lanes, thus being able to play the market more so than other lanes.

Retail use case No. 3: Evaluating which loads are best suited for conversion from truckload to intermodal.

Conversion from truckload to intermodal is about balancing cost and service. Is a potential 10%-15% savings in freight cost worth an extra day in transit? For intermodal to be viable, hauls need to be long, drays need to be short and lanes need density. SONAR has a unique volume data for rail intermodal that shows daily intermodal container volume by lane, market container size and loaded status. With intermodal density information on top of your existing freight flows, conversion opportunities begin to come into focus.

These are the 11 densest U.S. domestic intermodal lanes. SONAR shows the intermodal density (broken down by container size and loaded status) for every U.S. intermodal OD pair.

Of all transportation modes, intermodal is among the most imbalanced. As a result, the economics of intermodal shipping vary widely by lane. Comparing rate data across modes reveals where shippers can take advantage of excess capacity. SONAR contains intermodal spot rates for door-to-door movements of 53-foot containers, including fuel and all other surcharges (which is why SONAR intermodal rates can go bonkers during freight surges).

Comparing intermodal rates (blue) to truckload rates (yellow/green/orange) reveals: 1) little intermodal capacity in the LA-to-Dallas lane; 2) excess capacity from Newark to Chicago; and 3) a rational market from Chicago to Atlanta.

Shipping via rail intermodal can be risky because of variability in service levels. One extra day in transit relative to truckload may be OK, but a range of one to three extra days in transit is not. Intermodal tenders do not get rejected nearly as often as truckload tenders do, so when they do, it is a sign that intermodal networks are not running smoothly.

A warning to intermodal shippers in Chicago: Intermodal tenders outbound from Los Angeles and Memphis are being rejected less than 1% of the time, but in Chicago it’s more than 10%.

Retail use case No. 4: Deciding when to put your freight out to bid.

The importance of timing the bid cycle is vital to saving on transportation costs as putting out a bid when the market is tight will likely lead to higher contracted rates, thus putting pressure on the bottom line. Additionally, putting out a bid when the freight market is loose and there is capacity aplenty, low contract rates basically get thrown out when the market turns up and shippers are forced to pay higher rates through either mini-bids or the spot market.

Understanding the market dynamics compared to seasonal trends, though previous seasonal trends over the past 18 months have been thrown out the window due to the COVID-19 pandemic, allows for the decision-making around the bid cycle to improve. Understanding when freight volumes are typically strong compared to when markets tight relative to the norm.

(Source: FreightWaves SCI)

FreightWaves’ SCI shows historical rate trends along all lanes that are uploaded to the platform. Using the SCI score, when the score is high and the lane is easier to cover over time, looking at the historical rate along the Stockton-to-Chicago lane, which has a score of 71, shows that bids should be put out ahead of the summer months. The chart below shows OTRI, a measure of relative capacity, along the lane and shows that capacity tightens in the back half of the year, which signals that bids should be put out earlier to try and secure capacity at reasonable rates ahead of the traditional tightening that has upward pressure on rates.

(Source: FreightWaves SCI)

Retail use case No. 5: Using intelligence from SONAR in contract negotiations with carriers and 3PLs.

SONAR gives retailers insight into what carriers are seeing (load volumes by market and the relative attractiveness of destination markets) and how carriers are behaving (accepting or rejecting tendered loads). By mapping their freight flows into SONAR markets and lanes, retailers can begin to see where they have negotiating leverage. Carriers are far more willing to accept loads in certain lanes than others, and SONAR will help you break it all down.

Seattle to LA: An example of a backhaul lane where shippers have pricing leverage. Carriers are accepting more loads in this lane than most because: (1) there is relative looseness in the origin freight market; (2) the destination market is tighter than the origin; and (3) the destination market has far more outbound freight than inbound freight so it is easy for carriers to get reloaded.

Financial outcomes that improved freight market intelligence can deliver.

Transportation and logistics costs are typically included in retailers’ income statements within the Cost of Sales or Cost of Goods Sold line items, and therefore, directly impact the companies’ gross margins. The gross margin for large retailers varies widely by business mode but typically is in the 10%-35% range. Transportation costs as a percentage of retailers’ cost of sales can also vary widely and are, in general, inversely related to the value of the goods. The range we use in the analysis below is the assumption that transportation costs range from 1% to 5% of retailers’ cost of sales.

The charts above are intended to highlight the importance that reducing freight costs can have on a large retail chain. In the top chart, a retailer with a 25% gross margin may have freight costs that are the equivalent of 2.25% of revenue. Therefore, a 1% reduction in freight cost could save $225 for every $1 million in sales. That scales quickly when putting that in the context of retailers that do many billions of dollars in sales annually, such as those shown above.