With shippers ramping up sustainability efforts, the conversion of truckloads into intermodal units seems like a natural place to start. In addition to typically saving shippers 10%-15% in freight costs and halving the fuel surcharge, intermodal releases commensurately less greenhouse gas.

But, analyzing the real-world freight shipments of major CPG companies reveals the complications and constraints of that conversion process. Most truckload origin-destination pairs are incompatible with intermodal service because they are too short, not near a major rail terminal or cannot economically be moved in a dense intermodal corridor. Many other truckloads are simply too time-sensitive or service-sensitive for intermodal to be considered.

What’s also clear from analyzing shipment data is that many of the largest consumer goods shippers have already converted the most obvious applicable shipments to intermodal. For example, Shipper X (an aggregation of two household-name CPG companies) uses intermodal for ~90% of its dry loads in a number of dense long-haul lanes. As a result, we have avoided discussing the denest intermodal lanes like LA to Chicago and LA to Dallas in this report.

That’s not to say that intermodal conversion opportunities are no longer available, just that the largest CPG companies haven’t been sleeping on this. In this report, we highlight four lanes (Atlanta to Dallas, St. Louis to Harrisburg, Pennsylvania, St. Louis to San Bernardino, California, and Harrisburg to Jacksonville, Florida) where we recommend that Shipper X make greater use of intermodal than it already does. What those lanes have in common are long hauls, short drays and adequate density in addition to there being apparent room for additional intermodal conversion by this particular shipper.

We estimate based on different spot rate estimates contained in SONAR that Shipper X could save over $1,000/load in certain long-haul lanes by converting to intermodal. While the magnitude of that savings is partially due to a tight truckload market and heightened imbalances in domestic freight flows, our analysis suggests that intermodal conversion can go a long way toward offsetting the carbon impact of dry van shipments (offsetting the carbon impact of 45-plus dry van loads for every long-haul shipment converted to intermodal), if Shipper X wants to use the savings in that manner.

We review a major consumer goods shipper’s traffic flows (referred to as “Shipper X”) to evaluate how it could use domestic rail intermodal to: (1) save freight costs, (2) reduce fuel consumption and, thus, emissions of greenhouse gases, and (3) utilize that intermodal-related savings to fund the purchase of carbon tax credits to bring it closer to carbon-neutral.

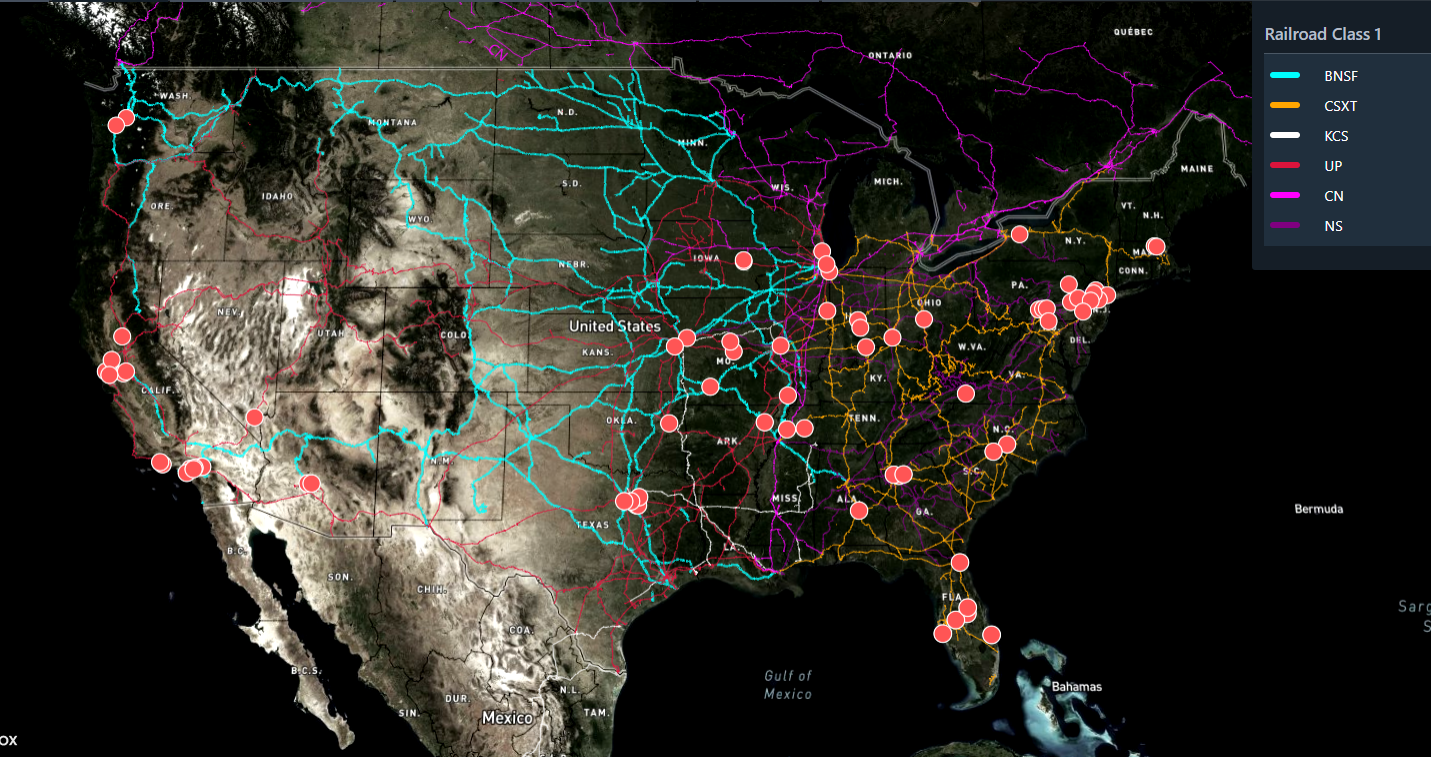

Shipper X’s shipment origins and destinations are shown with red dots in the map below. It has a concentration of facilities and warehouses in the Midwest and Mid-Atlantic regions. As a result, while there are some transcontinental freight movements, Shipper X’s freight movements are weighted toward truckload movements within a few hundred miles, including many intracity hauls. Those factors, of course, serve as limitations to converting truckloads into intermodal units.

(Source: SONAR, To learn more about FreightWaves SONAR, click here.)

Most of Shipper X’s freight is not compatible with intermodal.

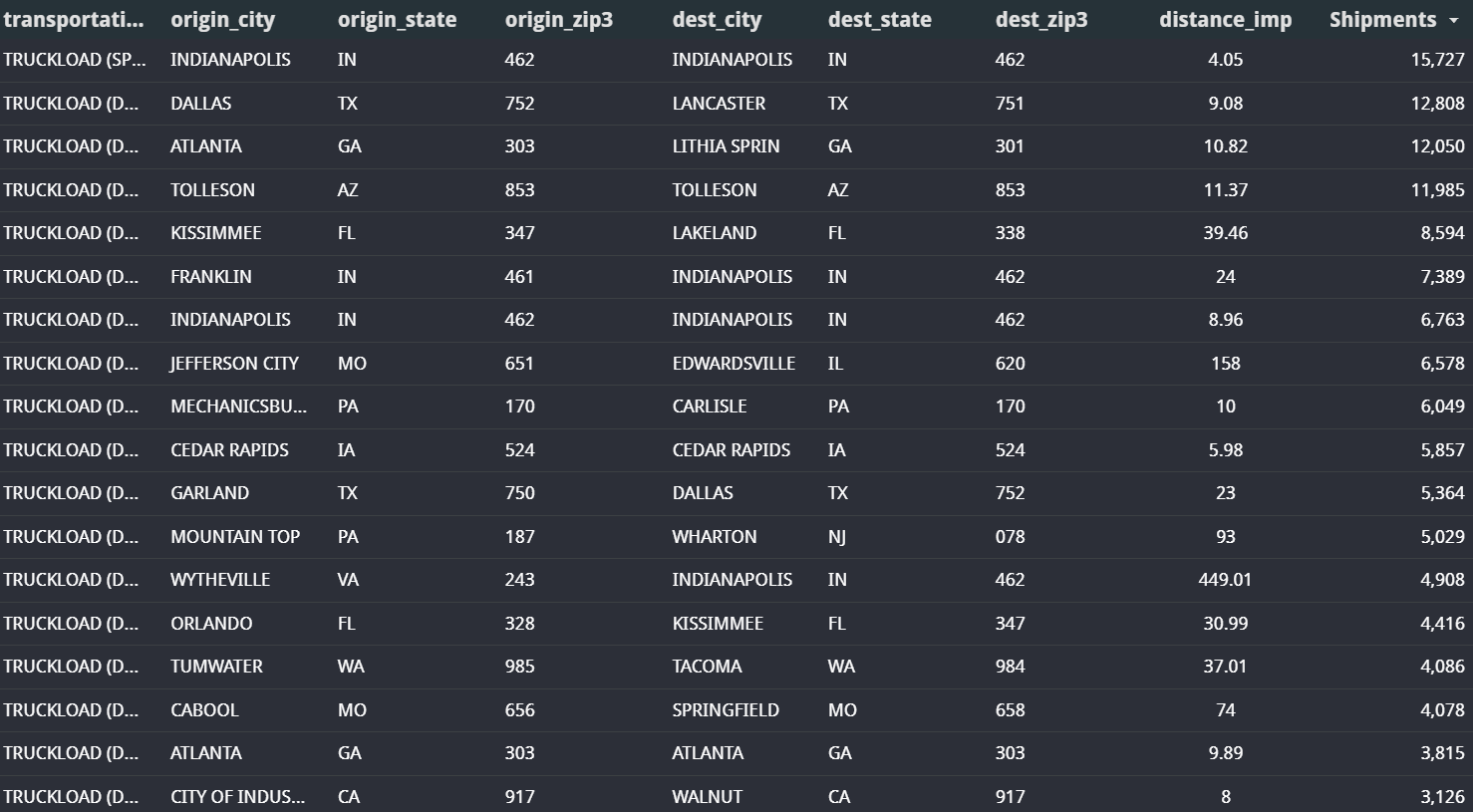

The chart below shows Shipper X’s freight lanes sorted by shipment volume. The lanes with the greatest volume tend to be within a single metro area, within the same state or have a destination that is in a state adjacent to the origin state. Of the 18 densest lanes shown below, only one lane (Wytheville, Virginia, to Indianapolis) is over 400 miles; that is still a poor candidate for intermodal conversion because a truckload shipment of that length can be completed in one day and it is not in a dense intermodal corridor.

Shipper X’s freight lanes, sorted by volume, show many short hauls.

(Source: FreightWaves data, To learn more about FreightWaves SONAR, click here.)

The data used in this analysis comes to FreightWaves from a transaction processor.

The transactions in this data set all took place in 2020, and multiple household-name consumer goods shippers are aggregated into a hypothetical “Shipper X.” We conducted our analysis in this manner to protect the anonymity of the shippers while keeping the real-world complexities that exist in a freight network.

In evaluating which lanes may be convertible from truckload to intermodal, we considered the following factors:

With that list of considerations in mind, in the following pages, we evaluate a handful of lanes where Shipper X is currently running significant truckload volume and walk through some thoughts on intermodal conversion.

Shipper X already uses rail intermodal heavily in numerous lanes anchored by at least one major freight market.

The lanes where Shipper X is already heavily using intermodal include many lanes that are inbound or outbound from the Harrisburg area (shown in the chart below of Newville, Pennsylvania, or Chambersburg, Pennsylvania). Harrisburg is known as a warehousing center and distribution point to much of the Northeast and Upper Midwest and is also one of the biggest nodes on the domestic intermodal network and one of the largest outbound freight markets.

Other intermodal lanes within the top 20 lanes utilized by Shipper X include cities or regions at either origin or destination that are among the major intermodal hubs, such as Chicago, Atlanta or Southern California (on the chart below at Rialto, California, and San Bernardino, California). In short, Shipper X is already using intermodal in the obvious places.

Shipper X is already using intermodal for long hauls to/from Newville (Harrisburg) and to/from major intermodal hubs.

(Source: FreightWaves data, To learn more about FreightWaves SONAR, click here.)

Shipper X is already using intermodal heavily in outbound Chicago lanes that exceed 600 miles. The company is using intermodal to move dry loads outbound Chicago destined for Newville (Harrisburg), Rialto and Jacksonville 91%, 89% and 88% of the time, respectively. That data excludes refrigerated and specialized loads. For those lanes, we conclude the remaining 9%-12% of dry loads that moved on the highway were likely too time-sensitive or too service-sensitive to utilize rail intermodal. They could have also taken place during a period of time last year when rail service was not up to the shipper’s expectation. We believe it is unrealistic to model a 100% conversion to intermodal on any lane because of the occasional need to move an expedited shipment.

Most dry outbound Chicago shipments already move via rail intermodal.

(Source: FreightWaves data, To learn more about FreightWaves SONAR, click here.)

Similarly, Shipper X is also making heavy use of intermodal in lanes that are inbound or outbound from the Harrisburg (Newville) area. Surprisingly, that includes many lanes with relatively short lengths of haul, such as Raeford, North Carolina, Suffolk, Virginia, and Cleveland, which are 388, 272 and 302 miles from Newville, respectively. That indicates to us that Shipper X is relatively far along in its intermodal conversion plans, and likely has a more efficient transportation network than most shippers.

Rail intermodal also dominates Shipper X’s inbound Newville (Harrisburg) loads.

(Source: FreightWaves data, To learn more about FreightWaves SONAR, click here.)

With that as background, we looked to identify lanes where Shipper X’s intermodal penetration has further room for expansion.

We did not see many lanes where Shipper X had left a clear major intermodal savings opportunity unturned. But, we did see several lanes where we believe there was still room for Shipper X to use rail intermodal more heavily.

We believe this approach has the advantage of knowing that intermodal is feasible in those particular lanes for this particular shipper. In other words, without knowing precisely where Shipper X’s facilities are located, we know that drayage routes from facility to rail head are not so long as to make intermodal service uneconomical. That said, we do not have visibility into the service constraints that could be a reason why the intermodal usage in a particular lane is not already higher.

Existing intermodal lanes where Shipper X could utilize intermodal more heavily

In these recommendations, we excluded lanes where the company’s intermodal penetration was already very high (85%-plus). We believe it is unrealistic to expect intermodal penetration to ever be 100% in a lane due to the occasional need for expedited service. We also assume that any freight with temperature requirements or specialized service requirements is not a candidate for intermodal.

Lane 1: Atlanta to Dallas

Rationale: When all locations in the Atlanta and Dallas metro areas are taken from the dataset, Shipper X is moving 51% of dry shipments via intermodal despite Atlanta to Dallas being a dense intermodal corridor. Those intermodal movements are concentrated specifically in the Atlanta-to-Lancaster, Texas, and Lithia Springs-to-Lancaster lanes, as shown in the table below.

Freight moving specifically from Atlanta to Lancaster is moving via rail intermodal, but that is not the case for most other loads from metro Atlanta to metro Dallas.

(Source: FreightWaves data, To learn more about FreightWaves SONAR, click here.)

There is sufficient intermodal density in the Atlanta-to-Dallas lane, as shown in the SONAR chart below at left. One caveat, however, is that spot rates have risen sharply in the lane to $2.44/mile, including fuel surcharges, which currently places them roughly in line with recent domestic truckload spot rates. That may mean that this is not the ideal time for intermodal conversions in this lane, but we believe it is a lane that Shipper X should continuously monitor.

Sufficient density exists in the Atlanta-to-Dallas lane, but intermodal rates have increased YTD.

(Source: SONAR, To learn more about FreightWaves SONAR, click here.)

Lane 2: Jefferson City (St. Louis), Missouri, to Newville (Harrisburg)

Rationale: Shipper X already uses intermodal heavily in this lane. In 2020, our data sample shows that the company moved 1,351 intermodal loads in the lane and 933 truckloads, so it used intermodal 59% of the time. The existing usage of intermodal shows that intermodal is viable given the location of its facilities. In addition, SONAR data shows that there is at least a moderate amount of intermodal density in the lane, with an average of about 80 domestic loaded containers moving in the lane in the past year.

(Source: SONAR, To learn more about FreightWaves SONAR, click here.)

Lane 3: Edwardsville (St. Louis), Illinois, to Rialto (San Bernardino)

Rationale: The company moved 1,769 intermodal units in the sample compared to 751 truckloads. Using intermodal for 70% of dry loads is a high percentage, but the 1,742-mile length of haul suggests that the intermodal economics in that lane may be compelling. In addition, intermodal spot rates shown in the comparable St. Louis-to-LA lane remain depressed at $1.14/mile including fuel surcharges given the backhaul nature of that lane.

(Source: SONAR, To learn more about FreightWaves SONAR, click here.)

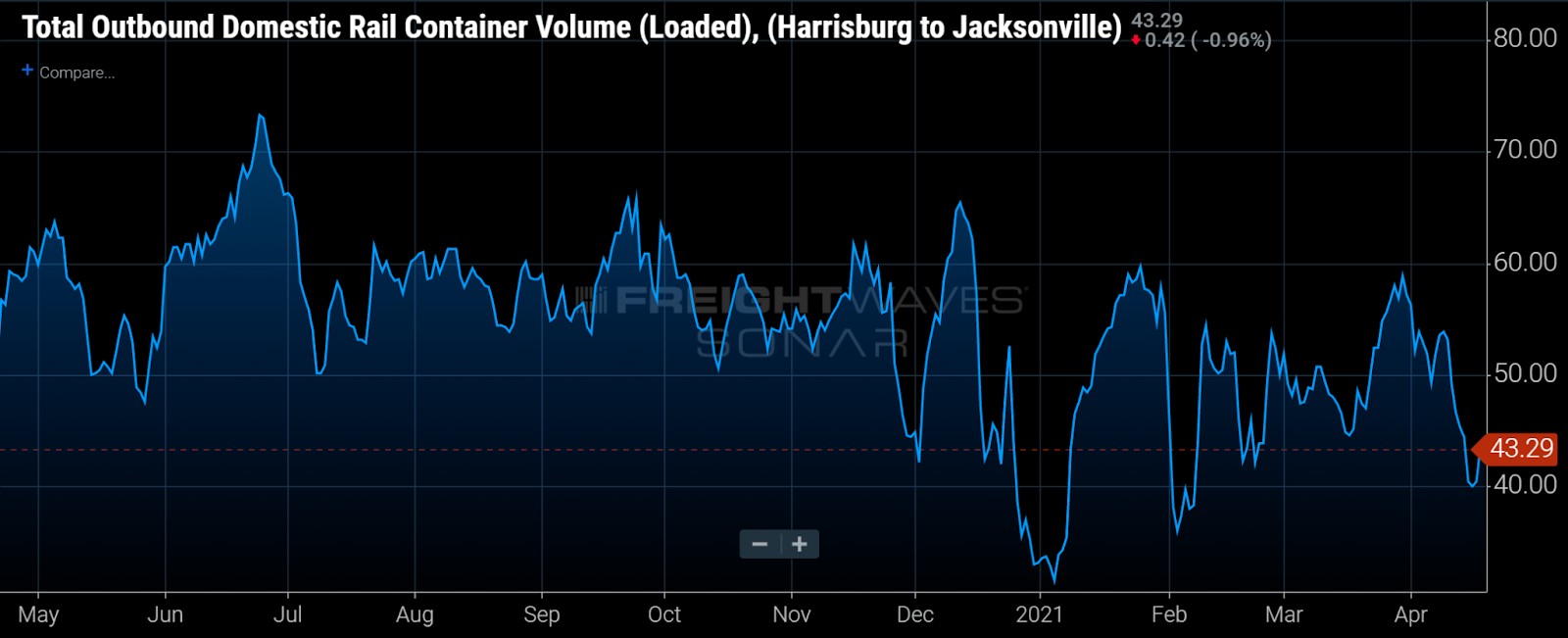

Lane 4: Newville (Harrisburg) to Jacksonville

Rationale: In the data sample, Shipper X moved 418 truckloads and 519 intermodal units in the lane, or utilized intermodal for 55% of dry loads. SONAR data suggests that there is sufficient intermodal density in this lane of 40-70 loaded domestic containers per day, on average. Utilizing intermodal in the lane also avoids high spot rates that carriers charge to compensate for the “Florida problem” of too few northbound loads out of Florida.

(Source: SONAR, To learn more about FreightWaves SONAR, click here.)

Current spot rates suggest that shippers can save $1,000/load in the key lanes we outlined and more in the backhaul westbound lane (i.e., St. Louis to San Bernardino).

The potential savings from intermodal conversion could go a long way toward offsetting the carbon impact on truckload movements, if the shipper wants to use the savings in that manner.

One caveat is that the spread between intermodal and truckload rates in the above chart is from different data sources and is above the traditional intermodal discount so the rate spread and savings may be higher than what a shipper may be able to achieve from intermodal conversions.