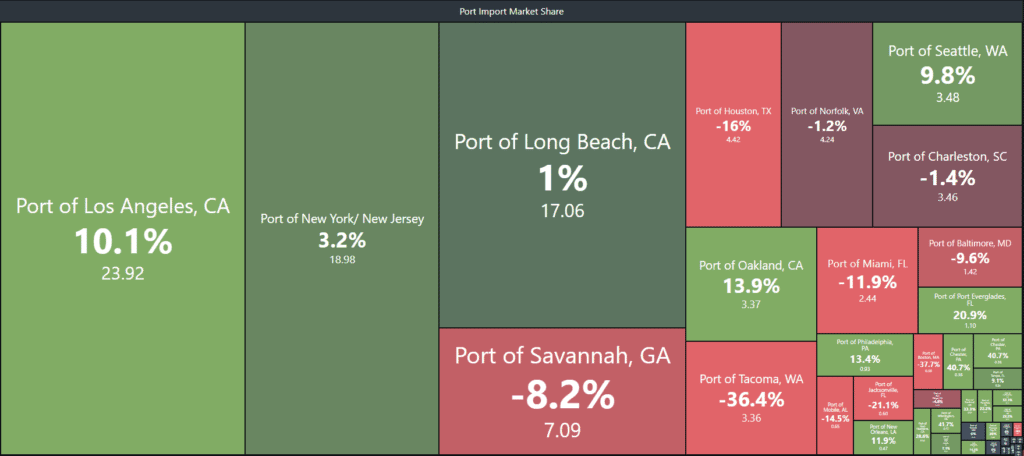

The ports of Los Angeles and Long Beach account for over 40% of the total maritime import shipment volumes. Image – SONAR Tree Map of import market share

The largest lanes for maritime imports originate in China and end on the North American West Coast, predominantly the ports of Los Angeles and Long Beach. As of last week, the Southern California ports handled over 40% of the shipments entering the U.S., creating new trouble for domestic freight management as these loads precipitate volatility in the OTR market.

According to this week’s chart, bookings for freight bound for alternative ports are increasing faster than LA and Long Beach. Given these are percentages of much smaller starting figures, the changes are significant against the backdrop of historic norms.

Not only are the ports infrastructures set up to handle a smaller amount of container volumes, but the surface transportation providers such as drayage, rail and truckload will also be tested as freight flow patterns disrupt network balance.

For drayage providers, this will simply be an abundance of demand that will inevitably push rates higher and keep them busier than normal. The amount of drayage capacity will directly impact what happens downstream to warehouses and trucking providers, potentially limiting or delaying their exposure to surging demand.

Rail networks were already tested last fall with heavy volumes moving from west to east, creating large imbalances. This new pattern may actually help even things out on their end with freight being more evenly dispersed. The big risk to rail in the long run if importers decide to push more freight into the East Coast ports is eliminating the cost advantage intermodal by rail has for long haul moves over 800 miles.

Yet, there’s always a bit of uncertainty, and this could mean lower volumes over time.

Truckload networks take a long time to build efficiently and drastic changes to domestic freight management and overall flows can wreak havoc on available capacity. Some markets may benefit from additional volumes. Northern California for instance is normally oversupplied in relation to the rest of the country with more freight entering than exiting the area. A growth in import volumes could help balance the markets as outbound demand rises.

Savannah, however, is on the opposite end of that spectrum. Savannah produces more freight than it consumes thanks to the port and a relatively low population density. Carriers will have trouble finding enough inbound loads to keep the market well supplied. Carriers will more than likely reposition trucks from Florida and South Carolina to meet the growing demand.

While these are nearby, they will also require “deadheading,” in which they move the truck without an active paying load, driving up the outbound rate.